The Fourth IMO GHG Study Executive Summary has been published. This study is the first iteration since the adoption of the Initial IMO Strategy on Reduction of greenhouse gas (GHG) Emissions from Ships in 2018, under which IMO Member States have pledged to cut GHG emissions from international shipping and to phase them out as soon as possible.

The study estimates that total shipping emitted 1,056 million tons of CO2 in 2018, accounting for about 2.89% of the total global anthropogenic CO2 emissions for that year. Under a new voyage-based allocation method, the share of international shipping represented 740 million tons of CO2 in 2018. According to a range of plausible long-term economic and energy business-as-usual scenarios, shipping emissions could represent 90%-130% of 2008 emissions by 2050.

For the first time, the study includes estimates of carbon intensity. Overall carbon intensity has improved between 2012 and 2018 for international shipping as a whole, as well as for most ship types. The overall carbon intensity, as an average across international shipping, was between 21% and 29% better than in 2008. IMO has been actively engaged in a global approach to further enhance ship’s energy efficiency and develop measures to

reduce GHG emissions from ships, as well as provide technical cooperation and capacity-building activities.

Highlights of the 4th GHG Study can be viewed at: https://www.imo.org/en/OurWork/Environment/Pages/Fourth-IMOGreenhouse-Gas-Study-2020.aspx.

Fourth Greenhouse Gas Study 2020: Emissions inventory

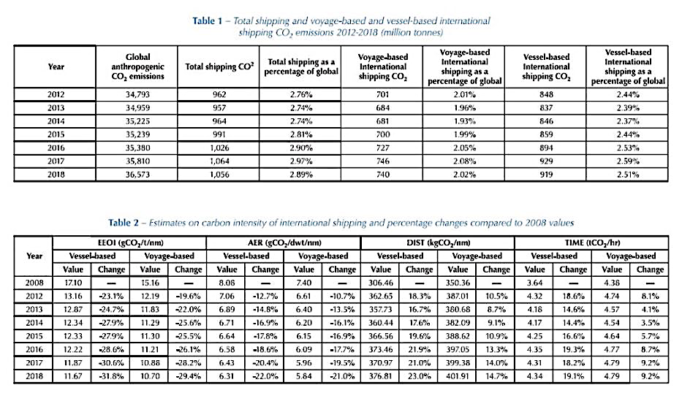

The greenhouse gas (GHG) emissions —including carbon dioxide (CO2), methane (CH4) and nitrous oxide (N2O), expressed in CO2e— of total shipping (international, domestic and fishing) have increased from 977 million tons in 2012 to 1,076 million tons in 2018 (9.6% increase). In 2012, 962 million tons were CO2 emissions, while in 2018 this amount grew 9.3% to 1,056 million tons of CO2 emissions.

The share of shipping emissions in global anthropogenic emissions has increased from 2.76% in 2012 to 2.89% in 2018. Under a new voyage-based allocation of international shipping, CO2 emissions have also increased over this same period from 701 million tons in 2012 to 740 million tons in 2018 (5.6% increase), but to a lower growth rate than total shipping emissions, and represent an approximately constant share of global CO2 emissions over this period (approximately 2%), as shown in Table 1. Using the vessel-based allocation of international shipping taken from the Third IMO GHG Study, CO2 emissions have increased over the period from 848 million tons in 2012 to 919 million tons in 2018 (8.4% increase).

Due to developments in data and inventory methods, this study is the first IMO GHG Study able to produce greenhouse gas inventories that distinguish domestic shipping from international emissions on a voyage basis in a way which, according to the consortium, is exactly consistent with the IPCC guidelines and definitions.

Projecting the same method to 2008 emissions, this study estimates that 2008 international shipping GHG emissions (in CO2e) were 794 million tons (employing the method used in the Third IMO GHG Study, the emissions were 940 million tons CO2e).

Carbon intensity 2008, 2012 – 2018

Carbon intensity has improved between 2012 and 2018 for international shipping as a whole, as well as for most ship types. The overall carbon intensity, as an average across international shipping, was 21% and 29% better than in 2008, measured in AER and EEOI respectively in the voyage-based allocation; while it was

22% respectively 32% better in the vessel-based allocation (Table 2). Improvements in carbon intensity of international shipping have not followed a linear pathway and more than half have been achieved before 2012. The pace of carbon intensity reduction has slowed since 2015, with average annual percentage changes ranging from 1% to 2%.

Annual carbon intensity performance of individual ships fluctuated over years. The upper and lower quartiles of fluctuation rates in EEOI of oil tankers, bulk carriers and container ships were around ±20%, ±15% and ±10% respectively. Quartiles of fluctuation rates in other metrics were relatively modest, yet still generally reaching beyond ±5%. Due to certain static assumptions on weather and hull fouling conditions, as well as the non-timely updated AIS entries on draught, actual fluctuations were possibly more scattered than estimated, especially for container ships.

Emission projections 2018 – 2050

Emissions are projected to increase from about 90% of 2008 emissions in 2018 to 90-130% of 2008 emissions by 2050 for a range of plausible long-term economic and energy scenarios (Figure 1).

Emissions could be higher (lower) than projected when economic growth rates are higher (lower) than assumed here or when the reduction in GHG emissions from land-based sectors is less (more) than would be required to limit the global temperature increase to well below 2 degrees centigrade.

Although it is too early to assess the impact of COVID-19 on emission projections quantitatively, it is clear that emissions in 2020 and 2021 will be significantly lower. Depending on the recovery trajectory, emissions over the next decades maybe a few percent lower than projected, at most. In all, the impact of COVID-19 is likely to be smaller than the uncertainty range of the presented scenarios.